Bookkeeping for Law Firms and Getting Trust Accounting Right

Most small businesses can survive messy books for a while. Tax season gets more expensive, some deductions get missed, and the owner pays a little more than they should. It is not ideal, but it is not catastrophic. Law firms do not have that margin for error.

When a law firm handles client money incorrectly, the consequences go far beyond a tax penalty. Commingling client funds with operating money, mishandling retainers, or failing to reconcile trust accounts can lead to bar complaints, malpractice claims, and loss of your license to practice. The rules around client funds exist for good reason, and they are enforced seriously.

Bookkeeping for law firms is different from other industries because of this compliance layer. Your books need to do everything a normal business requires, tracking income, expenses, payroll, and profitability, while also maintaining airtight records on every dollar held in trust. This post explains what trust accounting requires, where most firms get into trouble, and what basic controls keep your accounts clean and compliant.

Why Trust Accounting Changes the Rules

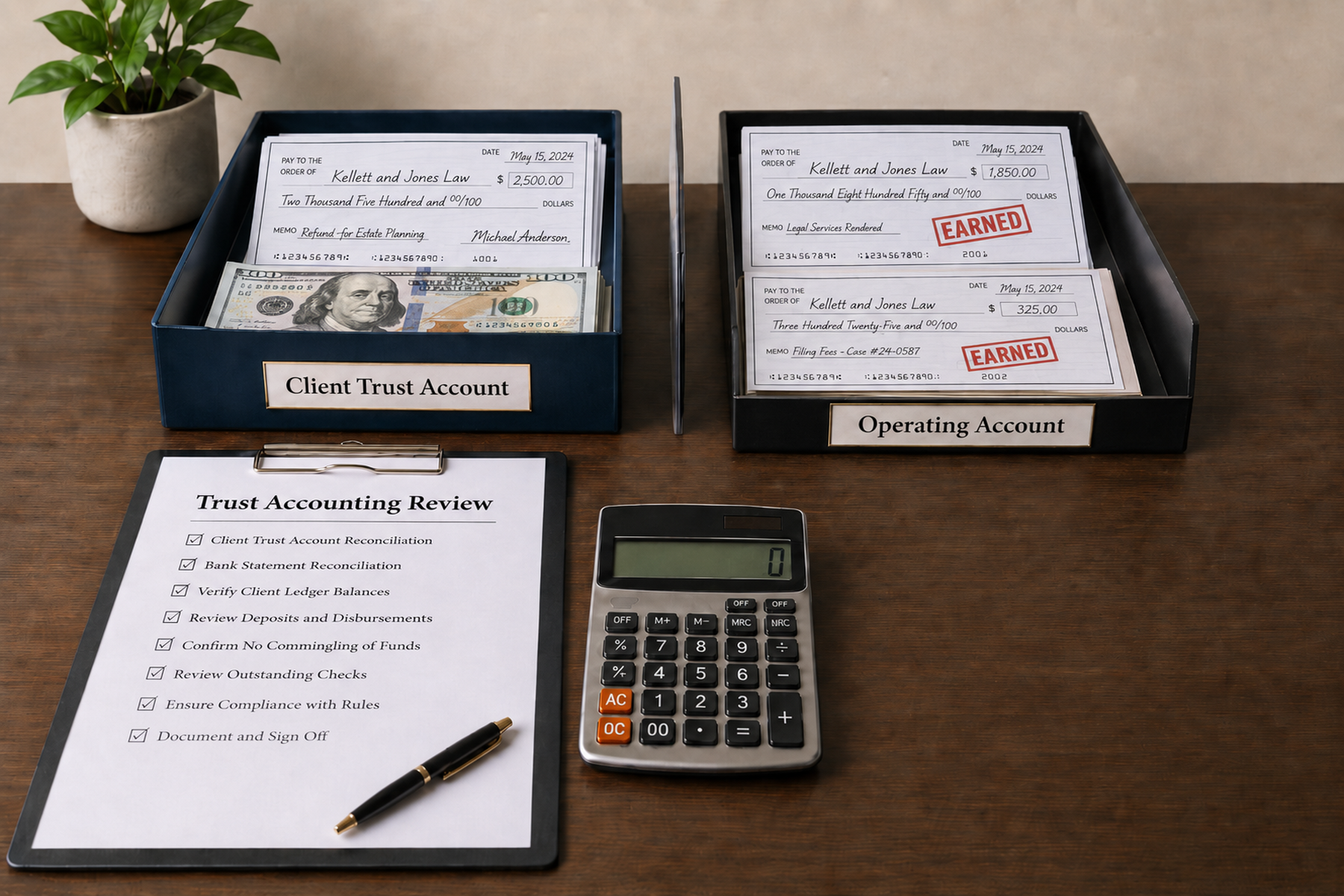

Every state bar has rules about how law firms handle client money. The details vary by state, but the core principle is the same everywhere: client funds are not your money. When a client pays a retainer, that money belongs to the client until you earn it. It must be held in a separate trust account, usually called an IOLTA account (Interest on Lawyers' Trust Accounts), and it cannot be mixed with your operating funds.

This is where law firm bookkeeping gets more complex than what a typical small business needs. You are essentially running two sets of books. Your operating account tracks the firm's own revenue and expenses like any other business. Your trust account tracks money that belongs to your clients. Every deposit, withdrawal, and transfer between those accounts has to be documented precisely.

The most common violation is commingling, which means mixing client funds with firm money. Sometimes this happens on purpose when a firm dips into trust to cover an operating expense. More often, it happens by accident. A retainer payment gets deposited into the operating account instead of the trust account. Earned fees sit in trust too long because nobody moved them. A refund gets processed from the wrong account. These mistakes may be innocent, but they still trigger the same compliance problems.

Three-way reconciliation is the standard for keeping trust accounts accurate. This means reconciling three things every month: the bank statement for the trust account, the firm's internal ledger for the trust account, and the individual client ledger showing what each client's funds should total. When all three numbers match, you know the money is where it belongs. When they do not, you have a problem that needs immediate attention.

Where Most Firms Run Into Trouble

The most common trust accounting mistakes are not dramatic. They are small process failures that compound over time. A retainer gets deposited into the wrong account. Earned fees do not get transferred to operating when they should. Client ledgers fall behind because nobody updates them after a billing cycle. A refund check gets cut from the trust account without adjusting the client balance.

These small errors create big reconciliation problems. When your monthly three-way reconciliation does not balance, you have to work backward through every transaction to find out why. If that process gets skipped for a few months, the backlog becomes serious. Some firms discover trust accounting discrepancies only during a random bar audit, and by that point, the cleanup is expensive and stressful.

Retainer management is another common trouble spot. When a client pays a $5,000 retainer, that money goes into trust. As you bill against it, the earned portion moves to operating. But when does that transfer happen? Some firms move money after each invoice. Others wait until the client approves the bill. The rules vary by state, and the timing matters. Fees that stay in trust too long create a false balance. Fees that get moved too early mean you are spending money you have not technically earned yet.

Firms that handle a high volume of trust transactions need bookkeeping that keeps pace with the activity. When trust accounting falls behind, even by a few weeks, the risk of errors increases significantly. Monthly reconciliation is the minimum. For busy practices, twice a month is better.

Basic Controls That Keep Your Accounts Clean

You do not need a complex compliance department to maintain clean trust accounts. You need a few consistent practices and someone who understands the rules.

First, keep your trust and operating accounts at separate banks if possible, and never at the same branch with the same login. This creates a physical and psychological separation that makes accidental commingling much harder. When transferring funds between accounts requires deliberate effort, mistakes happen less often.

Second, reconcile monthly without exception. The three-way reconciliation (bank statement, firm trust ledger, individual client ledgers) should happen within the first ten days of every month. If it does not balance, stop everything else and figure out why. Trust discrepancies do not get better with time. They get worse.

Third, document every trust transaction with a clear paper trail. Every deposit should note which client it belongs to and what it is for. Every withdrawal should reference the invoice or expense it covers. Every transfer to operating should match a specific amount of earned fees. If you cannot explain any single trust transaction in one sentence, your documentation needs work.

Fourth, limit who has access to the trust account. The fewer people who can deposit, withdraw, or transfer trust funds, the easier it is to maintain control. One or two authorized signers are enough for most small firms.

These controls sound basic because they are. The firms that get into trouble are rarely missing sophisticated systems. They are missing consistent habits. When the fundamentals happen every month without fail, trust accounting stays clean.

Know When to Bring in a Specialist

Law firm bookkeeping requires someone who understands both general business accounting and the specific trust accounting rules in your state. A general bookkeeper who handles retail shops and restaurants may be excellent at their job and still not understand IOLTA requirements, three-way reconciliation, or the timing rules around retainer transfers.

If your firm handles client funds regularly, your bookkeeper needs to know these rules or be willing to learn them thoroughly. The cost of getting trust accounting wrong is not a tax penalty. It is a bar complaint. That difference matters when you are choosing who manages your books.

If your current setup leaves you unsure whether your trust accounts are fully compliant, it is worth getting a professional review. Book a free consultation, and we will walk through your accounts and identify any gaps before they become problems.